You had some back taxes. You thought, “It is not a big deal. It can wait. They will not come after me.” But the debt kept growing year after year. Then came the penalties. And the interest. To fix this, you had set up an installment agreement. But then you made the same mistakes again. Now you are wondering if there is even a chance for a second agreement.

Many taxpayers do not understand how the agreements actually work. They hear “payment plan” and assume it is one-size-fits-all. But it doesn’t work that way. Different types come with different rules. And if you already have a wage levy, you need to navigate these rules carefully to avoid making things worse.

So let us break it all down, step by step, and figure out how to use these agreements to your advantage.

Key Takeaways

- Usually, the answer is no. Because the IRS prefers one agreement, but there are rare exceptions and different solutions.

- New tax debt will not trigger a second plan. You will need to modify your current agreement to include it.

- Business and personal tax debts may qualify for separate agreements, but only in rare cases.

- Failing to update your plan can lead to default, wage garnishment, or liens.

- Consolidating your tax debt is often the best move.

- Other relief options exist, like Offer in Compromise or Currently Not Collectible status.

What Exactly Is an IRS Installment Agreement?

An IRS installment agreement is a formal payment plan that allows you to pay off your tax debt in smaller, monthly payments instead of all at once. Be aware, however, these agreements do not erase your debt, but they can protect you from aggressive IRS collection (like levies, liens, or wage garnishment) while you pay it down.

Common Types of IRS Payment Plans

Depending on how much you owe and your financial situation, you may qualify for different types of installment agreements:

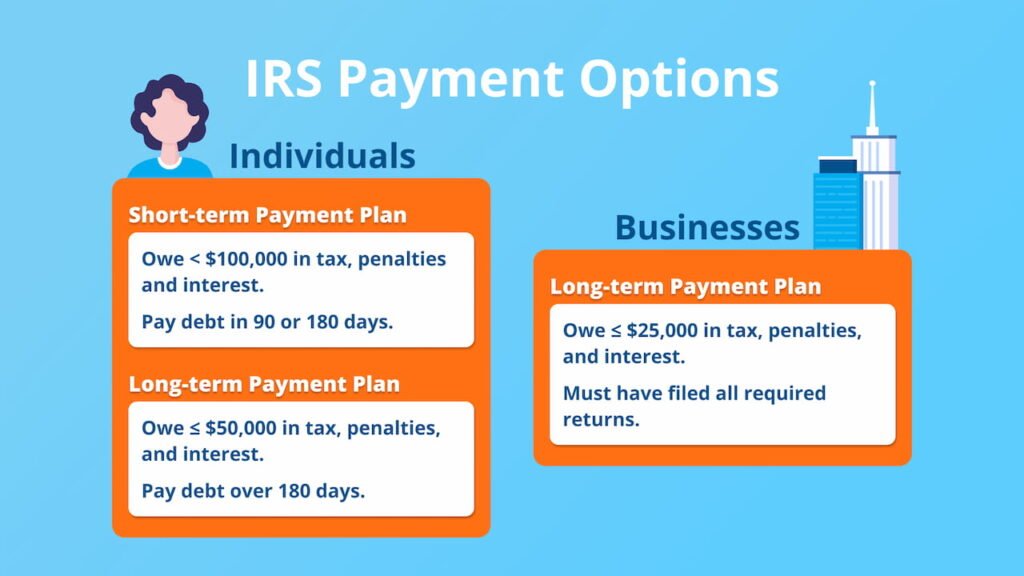

Guaranteed Installment Agreement

If you owe $10,000 or less (excluding penalties and interest), you likely qualify for this. You do not need to give the IRS a full breakdown of your finances. As long as you agree to pay off your debt within 36 months and stay current on future taxes, they usually approve it automatically.

Streamlined Installment Agreement

This is available for balances up to $50,000. Like the guaranteed plan, it does not require a full financial review. You will need to pay it off within 72 months (6 years), and you must agree to automatic direct debit payments if your debt is over $25,000.

Partial Payment Installment Agreement (PPIA)

It lets you make lower monthly payments based on what you can actually afford. You will need to provide detailed financial documents, and the IRS can review (and adjust) the plan every two years. It may not pay off the full debt before the statute of limitations expires, which means the IRS might not collect the entire amount.

Non-streamlined Installment Agreement

If you owe more than $50,000, or you cannot pay within the time limits of the streamlined plan, you will need a non-streamlined agreement. This requires full financial disclosure, bank statements, income, expenses, the works. It is a longer process, and the IRS may want to review your spending habits before approving the plan.

Installment Agreements Comparison Table

| Agreement Type | Who Qualifies | Max Debt Amount | Term Length | Financial Disclosure Needed? | Special Notes |

|---|---|---|---|---|---|

| Guaranteed Installment Agreement | Individuals who owe $10,000 or less (excluding penalties & interest) | $10,000 | Up to 36 months | ❌ No | Must file all returns and agree to stay current; almost always approved if you qualify. |

| Streamlined Installment Agreement | Individuals with total debt up to $50,000 | $50,000 | Up to 72 months | ❌ No (unless debt > $25,000, then automatic debit is required) | Fast-track approval; no detailed financials required. |

| Partial Payment Installment Agreement (PPIA) | Taxpayers who can’t afford full monthly payments | No cap | Varies | ✅ Yes | IRS may review your plan every 2 years; total debt may not be paid in full. |

| Non-Streamlined Installment Agreement | Those who owe more than $50,000 or can’t meet terms of other plans | Over $50,000 | Negotiable | ✅ Yes | Detailed review of income, expenses, and assets required; takes longer to process. |

Can You Have 2 IRS Installment Agreement Simultaneously?

IRS Rules on Multiple Payment Plans

In most cases, the IRS does not allow taxpayers to have more than one active installment agreement at the same time. If you have a new tax debt while already on a payment plan, the IRS will not create a second one. Instead, they will expect you to modify your existing agreement to include the new balance.

The IRS wants one plan, one payment, and no confusion.

Modifying Your Current Installment Agreement

The IRS does not automatically roll in new debt. You must contact the IRS to modify your existing installment agreement.

If you ignore your new debt, the IRS might view it as a breach of your original agreement, and they could cancel it. That opens the door for wage garnishments and other collection actions. Besides, new tax debt comes with its own baggage—more penalties and interest.

When Might the IRS Allow Multiple Agreements? (Special Exceptions)

It is rare, but there are limited exceptions. For example:

1. Business + Personal Debt

If you owe personal income tax and your business entity (like an LLC or sole prop) owes separate payroll or income taxes, the IRS may treat them as separate liabilities.

These are technically different taxpayer entities. You might qualify for an agreement under your Social Security number (SSN) and another under your Employer Identification Number (EIN).

However, the IRS still prefers consolidation, and will often push you to combine payments or dissolve one entity’s plan.

2. Divorce With Split Liabilities

If you and your former spouse both owe back taxes, and the IRS formally splits the debt due to a divorce decree or injured spouse relief, separate agreements may be allowed.

When it works:

- You filed jointly in the past.

- The court assigns each of your responsibility for different parts of the debt.

- You apply separately under your own SSNs.

You’ll need documentation. And the IRS may still try to collect jointly unless everything is legally separated and cleared.

Most taxpayers need to consolidate all outstanding balances into a single updated agreement. If you ignore a new debt while on a plan, the IRS can cancel the whole thing, and restart enforcement, including wage garnishment.

So, if you are juggling multiple debts, act fast. The longer you wait, the fewer options you will have.

What to Do if Multiple IRS Installment Agreements Are Not Possible

So, you cannot have two separate IRS payment plans. What now? No need to worry. You still have options.

- Consolidating Your IRS Debts into a Single Installment Agreement

Your first move can be updating the current agreement. This is called consolidation, and it simply means rolling all your unpaid balances into one monthly payment.

The IRS will recalculate what you owe and adjust your payment terms based on your total debt and what you can afford. This keeps you protected from enforcement actions, like wage garnishment or bank levies, as long as you stay current.

- IRS Offer in Compromise (OIC): Negotiating a Lower Debt

You might qualify for an Offer in Compromise. This is where the IRS agrees to settle your debt for less than you owe. It is not easy to get approved, but it is possible if you can prove that:

- Paying the full amount would create serious financial hardship

- You have filed all required tax returns

- You are not in an open bankruptcy case

You will need to submit detailed financial info, and the process can take several months. But for those who qualify, it can be a real lifeline.

Currently Not Collectible Status (CNC): Temporarily Pausing IRS Collections

If you are going through a tough time (like job loss, medical issues, or a major financial setback), you might be eligible for Currently Not Collectible status.

This does not erase your tax debt, but it pauses all IRS collection efforts, including garnishments and levies. You will still owe the balance, and interest continues to build, but it gives you space to recover without added pressure.

To qualify, you will need to show the IRS that you genuinely cannot afford to pay anything right now. And yes, they will want proof—income, expenses, and possibly bank records.

Dangers of Ignoring Additional IRS Tax Debts

- Without a court order, the IRS can garnish your wages. If they have suspicions, they might start taking a portion of your paycheck directly from your employer.

- If you owe the IRS and ignore it, they may place a federal tax lien on your home, vehicle, or other assets. This doesn’t mean they will take your house tomorrow. But it does mean they have a legal claim on it.

- IRS debt does not go away. It keeps growing. Over time, it can block loans, delay home buying, and keep you stuck in financial limbo for years.

Why Professional Help May Be Beneficial

Whether you are reviewing an existing agreement or starting from scratch, the IRS has options. But those options disappear if you delay. If you are unsure where to start, professional help is just a call away.

Struggling with multiple tax debts? Get free consultation now.